Structured settlements have become a cornerstone of financial security for many individuals who receive compensation from lawsuits, personal injury claims, or insurance settlements. Instead of receiving one large lump-sum payment, recipients are given smaller, scheduled payments over time, ensuring long-term financial stability. This beginner’s guide (2025 edition) is designed to simplify everything you need to know about structured settlements, including how they work, their benefits, and their potential risks. Whether you are an accident victim, a family member, or simply someone researching investment options, this guide will help you understand the fundamentals in a clear and practical way. By the end, you will have a solid understanding of structured settlements and how they may fit into your financial planning.

What is a Structured Settlement?

A structured settlement is a financial arrangement in which a claimant receives periodic payments instead of a one-time lump sum. These payments usually come from an insurance company through an annuity contract.

- Example: A car accident victim awarded $500,000 might receive monthly payments over 20 years rather than the full amount at once.

This ensures financial discipline, steady income, and reduced tax liability in many cases.

How Do Structured Settlements Work?

- Settlement Agreement: After a lawsuit or claim, both parties agree on compensation terms.

- Purchase of Annuity: The defendant (or insurer) purchases an annuity from a life insurance company.

- Periodic Payments: The annuity issues regular payments to the claimant (monthly, annually, or as agreed).

- Flexibility: Payment structures can be customized — e.g., larger amounts at specific times like college tuition or medical needs.

Advantages of Structured Settlements

- Steady Income Stream: Guarantees regular payments for years or even a lifetime.

- Tax Benefits: In many cases, payments are tax-free.

- Financial Security: Prevents recipients from spending everything quickly.

- Customization: Can be tailored to personal financial needs.

Disadvantages of Structured Settlements

- Lack of Liquidity: Hard to access lump sums when needed.

- Inflation Risks: Payments may lose value over time.

- Limited Flexibility: Once structured, terms cannot be easily changed.

- Selling Risks: Secondary market sales may result in losing value.

Who Benefits from Structured Settlements?

- Accident Victims: Provides long-term financial support.

- Families with Dependents: Ensures stability for children or spouses.

- Disabled Individuals: Regular payments cover medical and living expenses.

- Investors (Secondary Market): Opportunities to purchase at discounted rates.

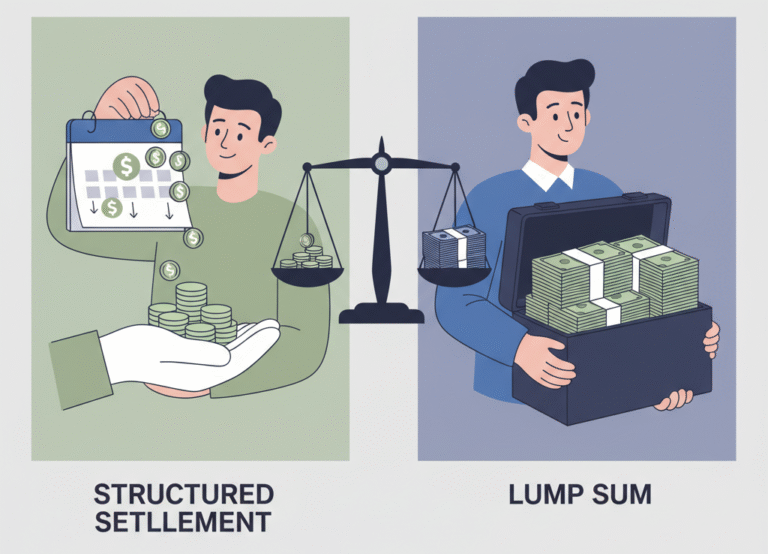

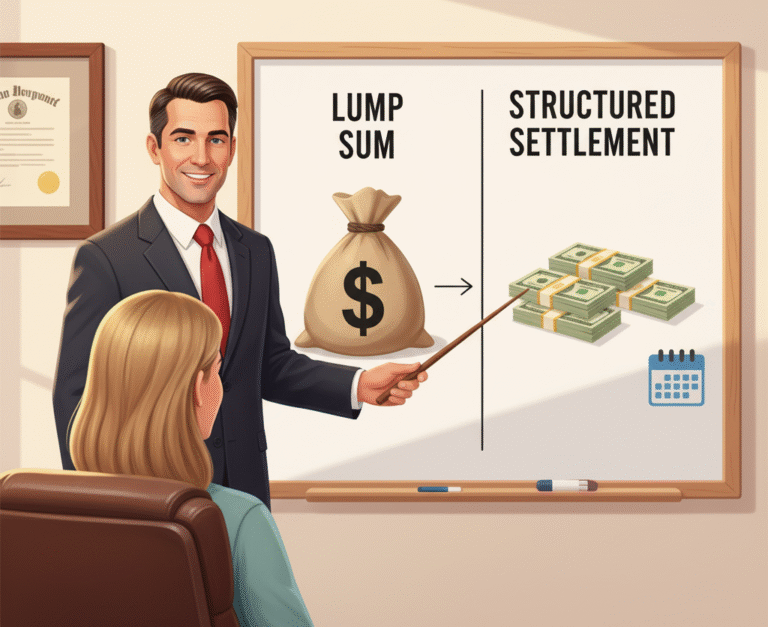

Structured Settlements vs. Lump Sum Payments

| Factor | Structured Settlement | Lump Sum |

|---|---|---|

| Risk of Overspending | Low | High |

| Tax Efficiency | Often tax-free | Potential tax burden |

| Flexibility | Limited | High |

| Stability | Guaranteed | Depends on management |

Tax Implications in 2025

One of the key reasons structured settlements remain attractive is tax efficiency. In 2025, most structured settlement payments remain exempt from federal and state taxes if tied to personal injury cases. However, investment in secondary markets may be subject to capital gains tax, depending on local regulations.

Common Myths About Structured Settlements

- Myth 1: “You can’t sell them.” → False. They can be sold with court approval.

- Myth 2: “They are always the best option.” → Not necessarily, depends on personal financial goals.

- Myth 3: “They are risky.” → False, since backed by large insurance companies.

FAQs

Q1. Can I sell my structured settlement?

Yes, but only through a court-approved process to protect your financial interests.

Q2. Are structured settlements only for lawsuits?

Mostly yes, but they can also arise from workers’ compensation claims.

Q3. What happens if the insurance company fails?

Most U.S. states have guaranty associations that provide protection up to certain limits.

Q4. Can I combine structured settlements with other investments?

Yes, many financial advisors recommend balancing them with other assets.

Expert Tips for Beginners (2025)

- Always consult a financial advisor before deciding.

- Compare the long-term security of structured settlements with the flexibility of lump sum payments.

- Understand state-specific laws and tax regulations.

- If selling, only work with reputable buyers approved by courts.

Structured settlements remain one of the most reliable ways to ensure long-term financial stability, particularly for individuals who may not be experienced with managing large sums of money. While they offer peace of mind, tax benefits, and security, it is essential to evaluate whether this payment structure aligns with your financial needs in 2025. By learning the basics through this beginner’s guide, you are now better equipped to make informed decisions about your financial future. Remember that every settlement is unique, and consulting a trusted advisor is always a wise step forward.