Investing is all about balancing risk and reward. For some, stocks and cryptocurrencies offer excitement, while others prefer bonds and real estate for stability. Somewhere in between lies a niche asset class that continues to grow in popularity—structured settlements.

In this article, we’ll explore the pros and cons of investing in structured settlements, giving you a clear picture of whether this alternative investment makes sense for your 2025 financial strategy.

📌 What Are Structured Settlements?

A structured settlement is a stream of payments awarded to a plaintiff after a lawsuit, typically involving personal injury, medical malpractice, or wrongful death cases. Instead of receiving a lump sum, the claimant gets regular payments funded by an annuity from an insurance company.

Investors can purchase these payment streams at a discount, effectively stepping into the shoes of the recipient and collecting the future cash flow.

📌 Pros and Cons of Investing in Structured Settlements

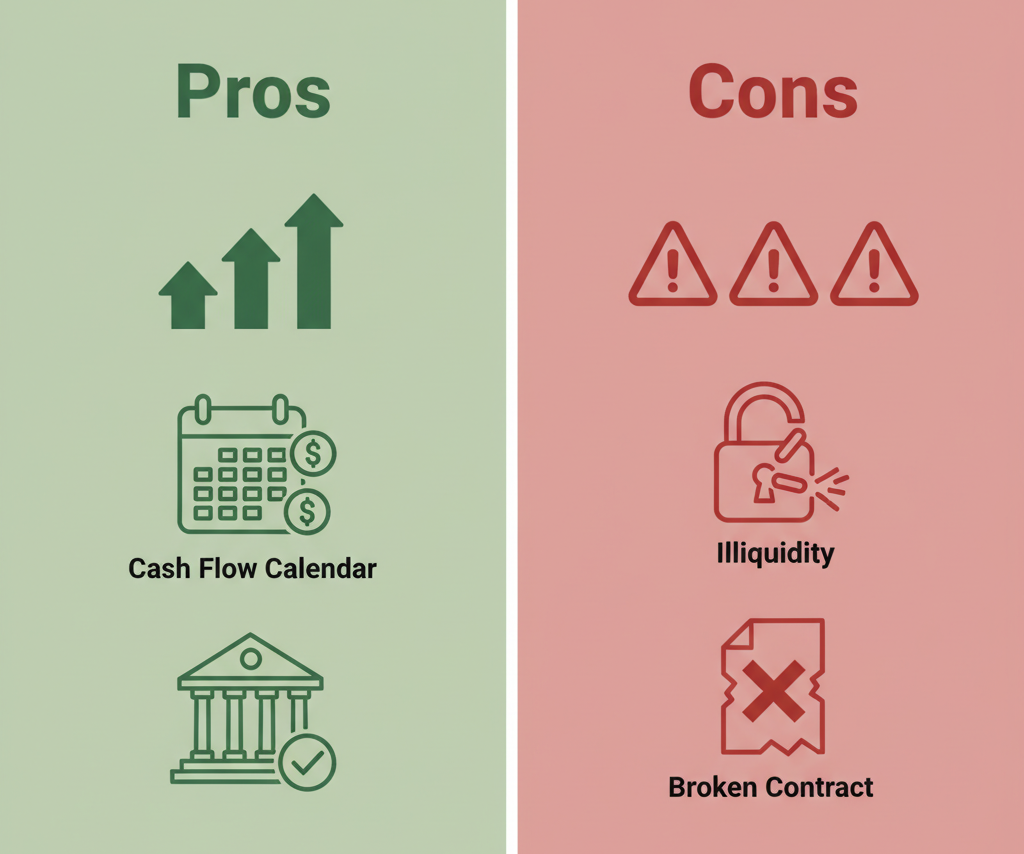

1. Predictable Income

Structured settlements provide fixed payment schedules—monthly, quarterly, or annual. For investors, this means stable cash flow that isn’t tied to stock market volatility.

2. Discounted Purchase Price

Because settlements are purchased at a discount, investors often achieve higher effective yields compared to bonds or CDs.

3. Legal Oversight

Every transfer must be approved by a court, which helps protect all parties from fraud or unfair deals.

4. Low Market Correlation

Unlike equities, structured settlements are not directly tied to economic swings. They perform independently of recessions, inflation, or stock crashes.

5. Portfolio Diversification

Structured settlements add an alternative asset class to a portfolio, helping balance risk across multiple types of investments.

📌 The Cons of Investing in Structured Settlements

1. Illiquidity

Once you purchase a structured settlement, it’s difficult to sell before maturity. This makes it unsuitable for investors who may need quick access to cash.

2. Credit Risk

Payments depend on the financial health of the insurance company. If the company defaults, payments could stop. This is rare but possible.

3. Complex Legal Process

Different states have unique requirements for settlement transfers. Investors must navigate varying legal frameworks.

4. Limited Access

Unlike stocks, structured settlements aren’t traded on public exchanges. Access usually comes through specialized brokers, making the market less transparent.

5. Potential Tax Issues

While many structured settlements are tax-advantaged, investors must verify whether the purchased settlement maintains that status.

📌 Key Factors to Evaluate in 2025

When weighing pros and cons, consider:

- Payment Timeline: Short-term vs. long-term payments impact liquidity needs.

- Discount Rate: A higher discount rate increases returns but may signal higher risk.

- Insurance Company Rating: Only purchase settlements backed by highly rated insurers.

- Court Approval Documentation: Verify all legal steps before purchase.

📌 Real-Life Example

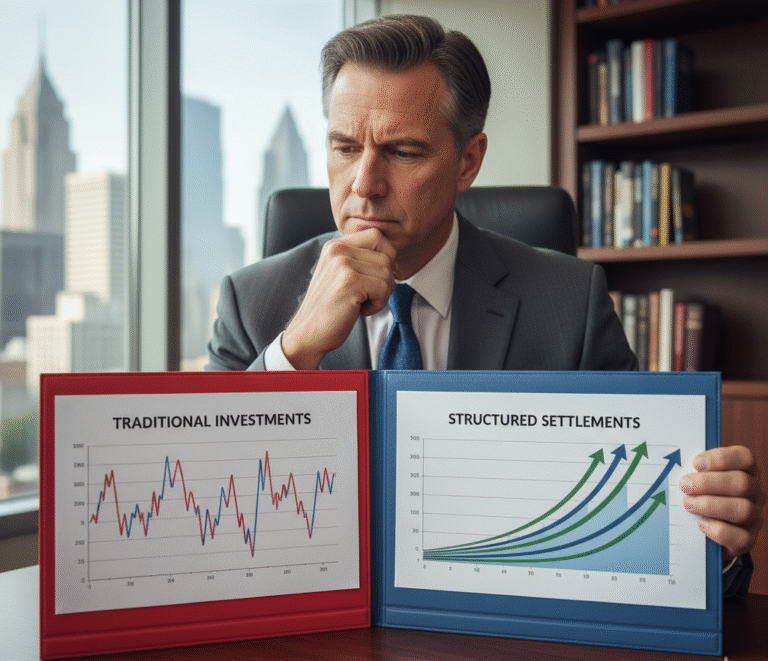

Imagine an investor buys a structured settlement paying $1,500 monthly for 15 years, totaling $270,000. If purchased at $200,000, the yield is highly attractive compared to bonds.

However, the investor cannot easily resell the settlement, meaning liquidity is locked for 15 years. This demonstrates the reward (higher return) but also the risk (lack of flexibility).

📌 Who Should Invest?

Structured settlements may be a good fit for:

- Retirees wanting consistent income.

- Conservative investors seeking safety over speculation.

- Diversifiers balancing volatile assets like stocks or crypto.

Not ideal for:

- Investors needing quick liquidity.

- People uncomfortable with long-term commitments.

📌 2025 Outlook for Structured Settlement Investments

With interest rates fluctuating and market volatility rising, structured settlements in 2025 remain attractive for steady-income seekers. More digital platforms now connect investors with court-approved settlements, making access easier than before.

However, regulations are tightening to prevent exploitation, so investors must work with reputable brokers.

✅ Conclusion

The pros of investing in structured settlements—steady cash flow, discounted prices, legal protection, and diversification—make them appealing for conservative investors in 2025.

The **cons—illiquidity, credit risk, legal complexity, and limited access—**must also be carefully weighed.

For the right investor, structured settlements can be a valuable part of a balanced, long-term financial strategy.